Planning Your Retirement Journey

When we spend time with investors, clients, or friends, we find that these topics concern people most: protecting their investments, retiring with enough money, planning for milestones, and knowing how much risk to take in this market. We'll take this opportunity to focus in on the hot topic of retirement in this blog.

Retirement: Do You Have Enough?

Recently, we posed some serious questions to our social media followers. We wanted to know what their retirement goals were and what they feared most about retiring.

Are you like some of them who are worried about outliving their retirement savings? Or might you be like some who wanted to make sure they spent it all in wonderful ways to the last breath?

Shallon Weis, CFP®, AIF® delivered truths about the road to retirement for attendees. Here are highlights of her insight on retiring with enough money that you can apply to your own retirement journey.

She suggests there are three stages of retirement:

- Saving for retirement

- Income during retirement

- Leaving your legacy to others

Saving for Retirement

Shallon advises investors to start early to take advantage of the potential growth of compounding. When you wait, you miss compound growth, the value of your investment growing because the gains and interest are earning gains and interest as time goes on. Consider her example:

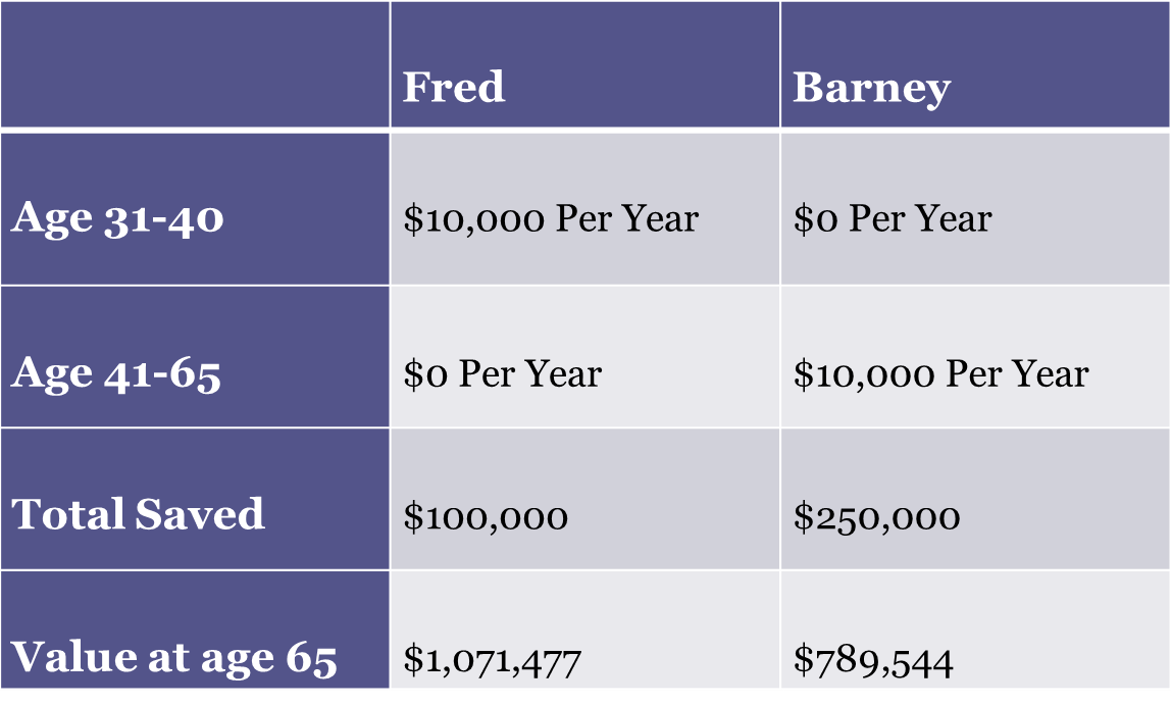

Fred and Barney are the same age. Fred invests $10,000 per year for 10 years and stops. Barney waits to begin investing until 10 years after Fred, then invests $10,000 per year for 25 years.

Assuming a hypothetical rate of return of 8 percent for both, Fred will have more money than Barney, despite investing significantly less overall. It's all about the power of compounding.

Beware of Obstacles. Common obstacles that could keep you from building a retirement nest egg are taxes, big expenses, inflation, and market fluctuation. how to build a portfolio and how to value financial assets.

Studies suggest we spend more on taxes than we do on necessities of food, clothing, and housing. You have options to help reduce the impact of taxes, like Tax Deferral Accounts which include 401(k), IRA, Roth IRA. Using tax-deferred accounts versus investing in a taxable account can help to minimize taxes throughout your lifetime and give your saving plan a boost.

Note: There are special IRS tax rules for these types of accounts and how much can be contributed or withdrawn annually. To learn more about these tax rules, contact Shallon.

Gaining control over your spending is a sure way to build that retirement nest egg, especially when it comes to big-ticket purchases. Before you jump into that purchase, visualize instead what that money might look like in the future. Are you willing to sacrifice now to save for the future? Let’s put it into play in this example:

The first big ticket item is a $60,000 boat, so instead of buying the boat you could invest into a taxable account and assuming an 8% return over 20 years and a 33% tax rate, you could have made $100,000. And if you put this into a tax-deferred account still assuming 8% return, you could have $279,657.

Simply stated, inflation is higher prices. If you think things get more expensive year over year now, consider the impact when you retire. This means your nest egg needs to grow faster than the cost of living, to provide enough money when you retire. That’s why it’s important to have investment strategies that can help grow the money you have saved, so you can have the lifestyle you dream of in retirement.

Investing in the markets is one strategy to grow your retirement nest egg. Let’s be honest, if you’re investing in the markets you need to get comfortable with highs and lows or market volatility. A lot of investors react emotionally when the markets turn down and take their money out and then wait too long to get back in. Following emotions can mean missing out of gains when the market rebounds. Having a financial plan can help address market volatility and your risk tolerance can help you not follow your emotions through the market cycles and keep you prepared for potential growth.

Income in Retirement

Once you’ve achieved that retirement goal, you begin drawing your income from the nest egg you’ve worked hard to build. But, to help your nest egg last as long as you and longer, it is important to remain proactive. Investing should not stop once you are retired, but rather shift to a different chapter. You are no longer working and saving, but now you are taking an income from your nest egg instead of a paycheck from your employment.

This is a critical part of our relationship at Bradford, we focus in on portfolio management, withdrawal rates, and capital preservation to help you protect your investment and retain income.

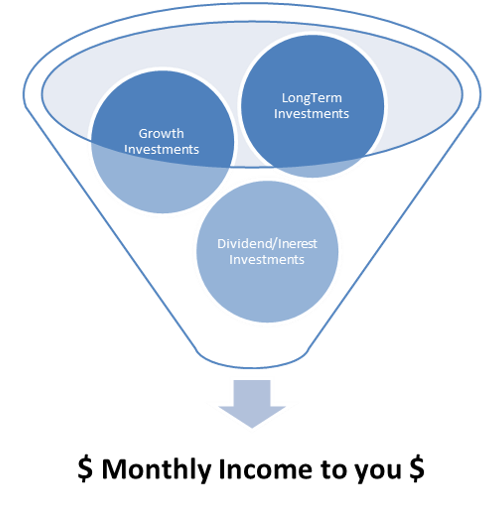

Let’s take a look at this example. So in this illustration, the retirement nest egg when Fred retires is $500,000. Fred has decided that he wants to take out $2,000 per month, which is 5% of his portfolio. To help keep up with inflation, we could invest 60 percent nest egg into growth type investments. These can help keep up with inflation. The other 40% we could invest in income-producing investments, such as investments that pay interest and dividends.

We do not want to have too much of your nest egg in fixed income investments, because you would have a higher chance of running out of money. However, putting too much into growth type investments could make your portfolio too volatile and scare you away at bad market times. There is also your tolerance for risk to take into consideration as well. It is important to have a financial advisor to help you with investing your nest egg.

Leaving Your Legacy

As you’re in retirement, many ponder what kind of legacy they will leave the next generation. Naturally, you want your estate plan to transfer your assets smoothly. That’s why it’s important to leave nothing to chance and make sure your Will or Trust reflects your wishes.

In addition to the Will or Trust, you will need to make sure that the beneficiary designations on your retirement accounts and life insurance have your desired beneficiaries. For example, on an IRA account typically the primary beneficiary is your spouse, but if your spouse passes away or you get a divorce, it is important to update your beneficiaries because it can cause needless expenses and taxes, or you could potentially disinherit your child or grandchildren, and it can cause delays in providing for the financial needs of your loved one.

Also keep in mind that your legacy priorities may change due to significant events in the lives of your loved ones, at which time you may want to update your designations.

Such life events may include:

- Change in marital status;

- Birth or adoption of a child or grandchild;

- Death in the family;

- Health problem;

- Relocation;

- New job or promotion.

For example, if one of your beneficiaries passes away before you do, what happens with their share? These are all life events that we need to keep in the back of our minds, so if something did happen, you can make the appropriate changes.

Speaking of tax-deferred accounts, such as an IRA – this next example is passing an IRA account down to your beneficiaries as we review options and optimizing their inheritance by saving taxes.

When someone other than a spouse inherits an IRA, they have four options:

1. Lump sum distribution. Taking the full distribution amount at one time.

2. Out-in-five. Taking the distribution out over a five-year period

3. Systematic withdrawal. Withdrawals over a specified period.

4. Stretch. Taking out the required minimum distribution over the beneficiary’s lifetime.

All of these options allow the beneficiary to withdraw from the IRA without the 10 percent penalty, however, the IRS always wants their tax money, and so all of these methods, the beneficiary will need to pay income tax on what they withdraw. Each method has its pros and cons.

No matter what stage of the retirement journey you are in, it pays to be informed, well planned, and tax efficient. Let’s discuss your goals further!