Understanding the K-Shaped Economy: What It Means for Your Financial Future

Over the past several years, economists and financial analysts have increasingly used the term “K-shaped economy” to describe what many Americans are experiencing firsthand: while some households and industries continue to grow and build wealth, others are facing rising financial pressure and uncertainty.

Unlike a traditional economic recovery, where most people move in the same direction together, a K-shaped economy creates two very different financial realities at the same time. One segment of the population experiences growth, opportunity, and increased wealth, while another faces challenges related to inflation, debt, housing costs, and financial instability.

For investors, retirees, business owners, and families planning for the future, understanding this economic environment is becoming increasingly important. The financial strategies that worked in a more stable and predictable market environment may need to evolve as economic divides widen and financial complexity increases.

At Bradford Financial Center, we believe thoughtful financial planning becomes even more valuable during periods of economic divergence and uncertainty.

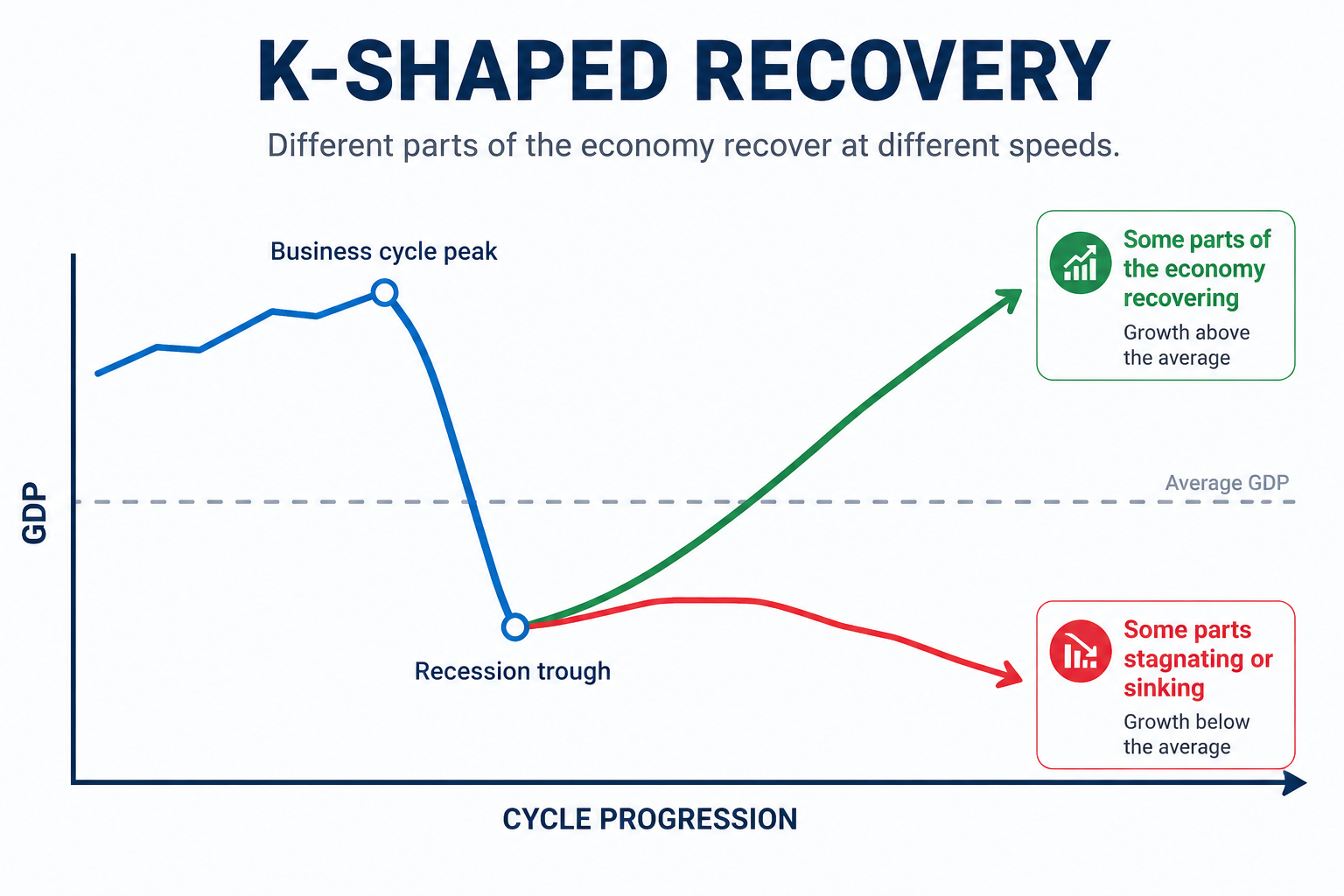

What Is a K-Shaped Economy?

The term “K-shaped economy” refers to an uneven economic recovery or market environment where different groups experience dramatically different financial outcomes.

Visualize the letter “K.”

- The upper arm represents individuals, businesses, and industries experiencing growth.

- The lower arm represents those facing economic decline or financial strain.

In today’s environment, many higher-income households have continued building wealth through:

- Stock market growth

- Home equity appreciation

- Business ownership

- Investments

- Higher savings rates

- Stronger wage growth in specialized industries

At the same time, many middle- and lower-income households are dealing with:

- Persistent inflation

- Rising insurance costs

- Increased borrowing expenses

- Higher housing costs

- Credit card debt

- Reduced purchasing power

This divide can create confusion because economic headlines may sound positive, while many individuals still feel financially stressed.

For example, the stock market may perform well while everyday expenses such as groceries, utilities, healthcare, and housing continue rising faster than many household budgets can comfortably absorb.

Why the K-Shaped Economy Matters to Financial Planning

One of the biggest challenges in today’s economy is that there is no “one-size-fits-all” financial strategy anymore.

Two families with similar incomes may experience completely different financial realities depending on:

- When they purchased a home

- Their level of debt

- Investment exposure

- Career field

- Retirement savings

- Tax strategy

- Healthcare costs

- Family obligations

This environment requires more personalized and proactive planning. Financial planning today is no longer simply about choosing investments. It increasingly involves coordinating multiple areas of your financial life together, including:

- Retirement planning

- Tax efficiency

- Risk management

- Estate planning

- Income strategies

- Cash flow management

- Long-term healthcare considerations

The more economic uncertainty and divergence increase, the more important it becomes to build a strategy designed specifically for your situation.

Inflation Continues to Shape Household Finances

Although inflation has moderated from its highest levels, many Americans are still feeling the effects of elevated costs in everyday life.

Areas such as:

- Property insurance

- Auto insurance

- Healthcare

- Utilities

- Home maintenance

- Food

- Property taxes

have remained stubbornly expensive in many regions.

For retirees or those approaching retirement, persistent inflation can create additional pressure on fixed income strategies and long-term withdrawal plans.

Even moderate inflation over time can significantly impact purchasing power.

For example:

- A retirement income plan built five years ago may now require adjustments.

- Healthcare and insurance costs may be growing faster than expected.

- Higher interest rates may affect borrowing, refinancing, or investment decisions.

This is why modern retirement planning must account for flexibility rather than relying on static assumptions.

Housing Has Become a Major Financial Divider

Housing is one of the clearest examples of today’s K-shaped economy.

Individuals who purchased homes before interest rates increased often benefit from:

- Lower mortgage rates

- Increased home equity

- Greater long-term stability

Meanwhile, younger buyers and renters may face:

- Higher monthly payments

- Limited inventory

- Rising rent costs

- Affordability challenges

Housing costs now impact many other financial decisions, including:

- Retirement timing

- Saving for college

- Investment contributions

- Relocation decisions

- Family support obligations

For many households, homeownership remains one of the largest components of long-term wealth building. That makes housing affordability and interest rates an important part of broader financial planning conversations.

Market Volatility and Emotional Investing

Periods of economic divergence often increase emotional reactions to financial headlines.

Some investors may feel pressure to:

- Move entirely to cash

- Chase high-performing sectors

- Make reactive decisions during market swings

- Delay retirement decisions

- Overcorrect after short-term volatility

However, emotional investing can sometimes create long-term setbacks.

A disciplined investment strategy built around your goals, risk tolerance, timeline, and income needs can help provide stability during uncertain periods.

This does not mean ignoring market conditions. Instead, it means making intentional adjustments within a broader financial framework rather than reacting to every headline.

For many investors, the focus today is shifting from simply growing assets to:

- Preserving wealth

- Creating tax-efficient income

- Managing downside risk

- Building long-term sustainability

The Growing Importance of Tax Strategy

Taxes are becoming an increasingly important part of comprehensive financial planning.

Many individuals focus heavily on investment growth while overlooking how taxes may impact:

- Retirement withdrawals

- Required minimum distributions

- Social Security taxation

- Capital gains

- Estate transfers

- Business succession

- Charitable giving strategies

In a more complex economic environment, tax-aware planning can play a major role in protecting long-term wealth.

Strategies such as:

- Roth conversions

- Coordinated withdrawal planning

- Tax-efficient investment placement

- Charitable giving structures

- Estate planning coordination

may help improve long-term outcomes when implemented thoughtfully and strategically.

Why Coordination Matters More Than Ever

One of the biggest trends in financial planning today is the shift toward integrated planning.

Historically, many people worked with separate professionals handling things like investments, taxes, insurance, and estate planning independently. Today, those decisions are increasingly interconnected.

For example:

- An investment decision may impact taxes.

- A retirement withdrawal strategy may affect Medicare costs.

- Estate planning decisions may influence long-term family wealth transfer.

- Business succession planning may affect retirement timing and income strategies.

Coordinated planning helps ensure those pieces work together rather than independently.

In a K-shaped economy where financial outcomes can vary dramatically from one household to another, coordination often becomes one of the most valuable parts of the planning process.

Planning for Confidence, Not Predictions

No one can predict exactly how markets, inflation, interest rates, or the broader economy will evolve over the next several years.

But successful financial planning is not built on perfect predictions. It is built on preparation, flexibility, and thoughtful decision-making.

The goal is not necessarily to eliminate uncertainty. The goal is to create a strategy capable of adapting as life and the economy change.

That may include:

- Stress-testing retirement income

- Reviewing risk exposure

- Updating estate documents

- Evaluating insurance coverage

- Building liquidity reserves

- Adjusting tax strategies

- Reassessing long-term goals

Economic environments will continue evolving. Financial plans should evolve with them.

Moving Forward in Today’s Economy

The K-shaped economy highlights an important reality: financial experiences are becoming more individualized than ever before.

That means personalized guidance, coordinated planning, and long-term strategy may play a larger role in helping individuals and families navigate uncertainty with greater confidence.

At Bradford Financial Center, we believe financial planning should help simplify complexity and provide clarity during changing economic environments.

Whether you are preparing for retirement, evaluating your long-term investment strategy, planning for future generations, or simply looking for greater confidence in your financial direction, a thoughtful plan can help you stay focused on what matters most.